First Aid Kit is a newsletter meant to help you fight a brutal enemy — the American health care system. Subscribe here.

Buying your own health insurance? Healthcare.gov. Full stop

Health insurance you can buy on healthcare.gov is crappy in the usual ways. Everything else is worse.

November 30, 2021

Share

Hey there—

Lots of folks have strong opinions about the Affordable Care Act; I’m not here to get into that fight.

But: Right now, if you are buying health insurance for yourself, healthcare.gov is your best bet.

Of course, no matter where you buy it, health insurance sucks. Profit-seeking insurance companies are a big source of evil. (In future installments, we’ll spend a lot of time talking about how to fight them.)

So, yes: Health insurance you can buy on healthcare.gov is crappy in all the usual ways.

Everything else is worse. Even when offered in good faith, the “alternatives” can leave you wide open to financial ruin. And they are not always offered in good faith.

So strap in for some scammy stuff, but stay with us for some not-so-bad news.

Why is everything else worse?

The Affordable Care Act has rules about what insurance has to cover. (Like, preventative care, mental health, prenatal and maternity care, pre-existing conditions, etc.). Plans on the marketplace (and most employer-sponsored insurance) have to follow those rules.

Every other type of plan is what experts call “junk” insurance.

Just ask the college professor who got half her foot amputated and was told by her insurer, “Nah, we’re not paying.” So give junk insurance a hard pass.

Do “Health Care Sharing Ministries” count as junk insurance?

Personally, I would say they’re worse (even though I know people who use/like them). They’re not insurance at all. Which can sound like a selling point — because, yes, health insurance sucks — but it’s not. Here’s why.

-

Many of these outfits won’t even accept lots of folks — like LGBTQ+ people or single parents

-

Many of the caveats about junk insurance plans — how they exclude things like pre-existing conditions, mental health, etc. — apply here.

-

If they ever decline to pay for something — and they often do — you’ve got zero recourse.

When you buy insurance from Aetna, Cigna, etc., you have a contract in which they promise to pay for certain things. Government regulators (and lawyers, and others) can help you enforce that contract. Not an option with health care sharing ministries.

HBO’s John Oliver1 did a takedown about sharing ministries, and here’s his most-damning bit of evidence:

The number of Better Business Bureau complaints against Liberty Healthshare was a lot higher than the number of complaints against the much-bigger Cigna. “Imagine having more people complain about you than about Cigna.”

In the most hair-raising case I know of, a health-sharing ministry was clearly acting in good faith. They paid $50,000 for a hernia repair — way more than the operation typically costs. But this particular hospital charged even more. The patient got stuck with a $67,000 tab.

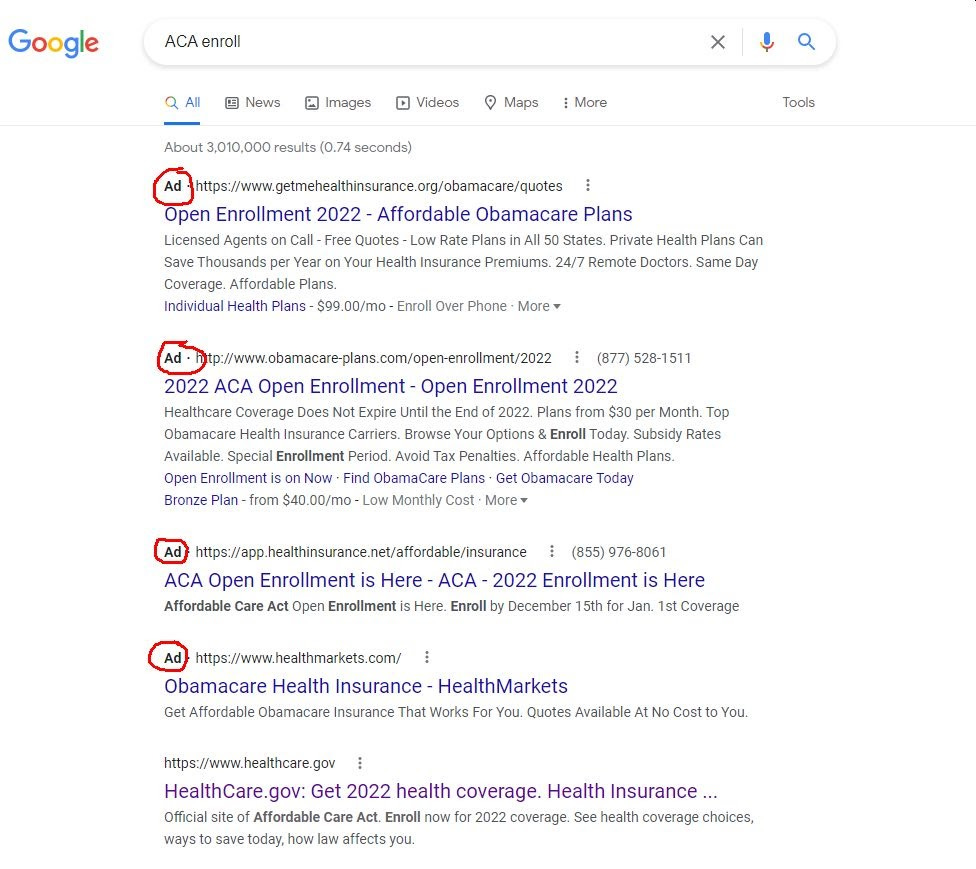

Now, in your search for ACA-compliant health insurance…do not trust Google.

A lot can go wrong if you do.

This fall, Georgetown University researcher Dania Palanker searched terms like “ACA enroll” and “Obamacare enroll” on Google, and got super-junky, often-scammy results. They looked like this:

Without the word “Ad” circled in red, those first results all looked pretty legit. But they weren’t.2

Palanker followed those links, typed in a name and phone number, and soon got deluged with calls from folks looking to sell her junk insurance.

They were telling her things that weren’t true, like ACA-compliant plans would be super-expensive for her. FALSE. At least for this year. (More on that shortly)

For a detailed account of how this kind of encounter can go down, check this account from journalist Oliver-Ash Kleine.

Result: They ended up railroaded into a Health Care Sharing Ministry plan, which they very much did not want. To get out of the deal, they canceled their credit card!

‘Healthcare.gov’ will take you to the right place. (Another option is healthsherpa.com, which sells only ACA-compliant plans; the web design is different, and if you like it better, you’re in OK hands here.)

So you’re on board. Let’s share some better news.

Bargains are available on healthcare.gov this year.

If you’ve looked in previous years and thought, “Yikes, that’s expensive!”— look again.

Last spring’s American Rescue Plan included huge subsidies for most people buying insurance through Obamacare exchanges. Millions of people qualified for free health insurance. Premiums = $0.00.

Those folks also qualified for giant subsidies on actual health care: All the co-pays, coinsurance, out-of-pocket stuff that normally make health insurance so crappy were dramatically shrunk down, an incredible deal.

(To get the subsidies on actual health care — the technical term is “cost-sharing reductions”— you need to pick a Silver plan.)

Those subsidies apply to anyone making less than 250 percent of the federal poverty level. For a single person, that threshold is just over $32,000 a year. A lot of people meet that: More than 44 percent of workers earn less than $30,000 per year.

And no matter what your income, the subsidies bring premiums down a bunch.

When they came out last spring, insurance broker Sheron Sidbury told me she saw results.

“Every time I’ve run an application I’ve been able to smile,” she said. “It wasn’t like the other years, where I wanted to cry with them.”

For example: One couple saved more than a thousand dollars on their monthly premium. “Unsubsidized, they were over $2,000 a month, and the husband was like, ‘No way,’” Sidbury said. “But I called him back this month and they got it down to $949.”

And all those subsidies? They’re still in effect. They apply to health insurance you can buy right now for 2022.

OK, but how much for me?

The numbers are complicated, and they vary from state to state. You can:

-

Actually go shopping on healthcare.gov

-

Make yourself an estimate: Start with this online subsidy calculator. Then you can preview the prices of different plans to see the non-subsidized price and do your own math.

So, where’s the bad news?

Well, there are folks who miss out and can’t get a subsidy on the ACA marketplace.

-

Your employer offers “affordable” health insurance: Technically “affordable” means you pay less than 9.61% of your household income for it—then you can’t get an ACA subsidy.

-

Worse, you get caught in the “family glitch”: That “affordable” measure for employer coverage? It only applies to coverage for an individual employee. If you’ve got family members who also need insurance … it doesn’t matter how much that insurance costs you.

-

So, say you make $55,000 a year. Insurance-for-you means paying $5,000. That’s “affordable.” Insurance-for-the-family means paying $15,000? Still technically “affordable.” That’s the glitch. Fun, huh?

-

-

You get caught in the Medicaid gap. The ACA expanded Medicaid, so if you earn less than 100% of the federal poverty level, then you qualify for Medicaid instead. EXCEPT: States had to say yes to that expansion, and not all did. In the 12 states that didn’t expand Medicaid, only very-limited groups qualify for Medicaid. 2.2 million people get caught in that gap.

OK! This concludes our series on picking health insurance. We’ve got our normal list of resources below. If you’re eager for more, we’ve got a podcast for that!

We still have some more for you before the end of the year!. So stick around.

Till then, take care of yourself,

Dan

P.S. We’ve been talking about great deals in this edition. Here’s one more: Support our work and a program called NewsMatch means any donation you make to us will get matched.

So please, during this Week of Giving: Step right up and donate! You’ve got five bucks? They’ll turn it into ten. You’ve got $100? They’ll make it $200.

And if you make a monthly pledge, they’ll match 12 months’ worth, upfront: Sign up for $5 a month, and they’ll give us $60 right away.

SUCH A DEAL, RIGHT? Sign up for any amount — a one-time gift or a monthly donation — right here.

Resources

-

Here’s a story from friend-of-the-show Celia Llopis-Jepsen about those assisters and those subsidies in Kansas.

-

Our pals at Georgetown did a “secret shopper” survey and got hammered by spammers and scammers, so you don’t have to. (Here’s a less-academic write-up.)

-

More horror stories! Well-educated Peace Corps vet here: He Bought Health Insurance for Emergencies. Then He Fell Into a $33,601 Trap. Yep, “junk” insurance strikes again.

-

Here are some other “alternatives” that you might want to be wary of.

1

Full and PROUD disclosure: An Arm and a Leg’s editor, Marian Wang, is a senior producer for John Oliver’s show. She didn’t work on this particular segment, but she is amazing.

2

Google results used to be even worse! Newspapers have documented problems and members of Congress have complained about them for a long time, so Google made some adjustments in 2019.

Get the First Aid Kit Newsletter!

Summing up the practical lessons we've learned about surviving the health-care system, financially.

Reporting on why health care costs so freaking much, and what we can maybe do about it.

More about us →

First Aid Kit

Get our latest tips for dealing with the healthcare-industrial complex.

Have a health care question?

For topic-specific deep dives and recommended reading, start here or use the search bar below to explore our site.