First Aid Kit is a newsletter meant to help you fight a brutal enemy — the American health care system. Subscribe here.

Preventive care: what does (and very likely doesn’t) count

And what to do if you get a bill you don’t owe.

January 22, 2026

Share

Hey there,

A couple weeks ago, we made the case for getting your annual checkups early this year.

Most of us think of these checkups as “preventive care” — the kinds of services that the Affordable Care Act says your insurance company needs to cover 100%, even if you haven’t met your deductible.

But we get lots of emails from pissed-off listeners wondering why they’re looking at a bill for something that sure seemed like “preventive care.”

So what actually counts? Is the whole checkup covered? What about blood work?

It turns out: What counts as preventive care is fairly limited — and a bit confusing.

When it comes to ringing up your bill, two things end up working against you: Your health care provider has incentives to add on more charges, and your insurance plan will, as always, look for ways to not pay.

It’s a medical-bill minefield. Here’s what to know going in, and when to pick a fight over your bill.

Here’s what’s (supposed to be) 100% covered

The feds have a list of services — or, actually three lists. One for kids, one for all adults, and one for women.

Guess what’s not on the “all adults” list? A basic yearly checkup.

So “well child” and “well woman” appointments are covered.

For everything else, what’s covered depends on your age and other risk factors.

Examples for adults include:

- Certain blood tests, like for cholesterol, diabetes, and HIV

- Immunizations

- Screenings for breast, cervical, and colon cancer and mental health conditions like depression

- Birth control

Check the list for your age and gender — and the details. Cholesterol drugs like statins are covered for some adults. Same with PrEP, the HIV-prevention medication.

And of course: All of this only applies if your provider is in-network with your insurance plan.

Why you might get a bill anyway

Your doc isn’t in-network. Or your doc is in-network, but the lab they send your tests to isn’t.

That second part is something you want to be especially careful about. This actually happened to Dan: He got charged hundreds of dollars for a Vitamin D test when his doctor’s office sent the test to an out-of-network lab. Ouch.

Your screening is “diagnostic” rather than preventive.

This is a big one. For something to count as preventive, it has to be a test done in the absence of symptoms and within certain timelines. A common example: a routine colonoscopy vs. a colonoscopy because you’ve been having digestive issues.

Your doctor’s office tacks on an “office visit” or “facility” fee.

Yep, they’re totally allowed to do that. And unfortunately, federal rules say insurance plans have a lot of leeway in deciding whether to cover it.

Before you head in, ask the staff whether you can expect one of these charges. As we’ve reported, you’re most likely to get socked with a facility fee if a hospital owns the medical practice.

Your doctor orders screenings that aren’t within federal guidelines.

For instance, if your doctor orders up a complete blood count panel. Some of the tests are not on the list, and you could get a bill.

Same if they also order diagnostic tests or tests to monitor a chronic condition. That’s what happened to a patient profiled last year in KFF Health News’ Bill of the Month.

You bring something else up at the appointment.

Remember: Your doctor has every incentive to bill you for any and all care that happens during an appointment — so if you mention that your knee has been bothering you, or you’ve been having trouble sleeping and wonder what they might recommend… they could bill you for a consult.

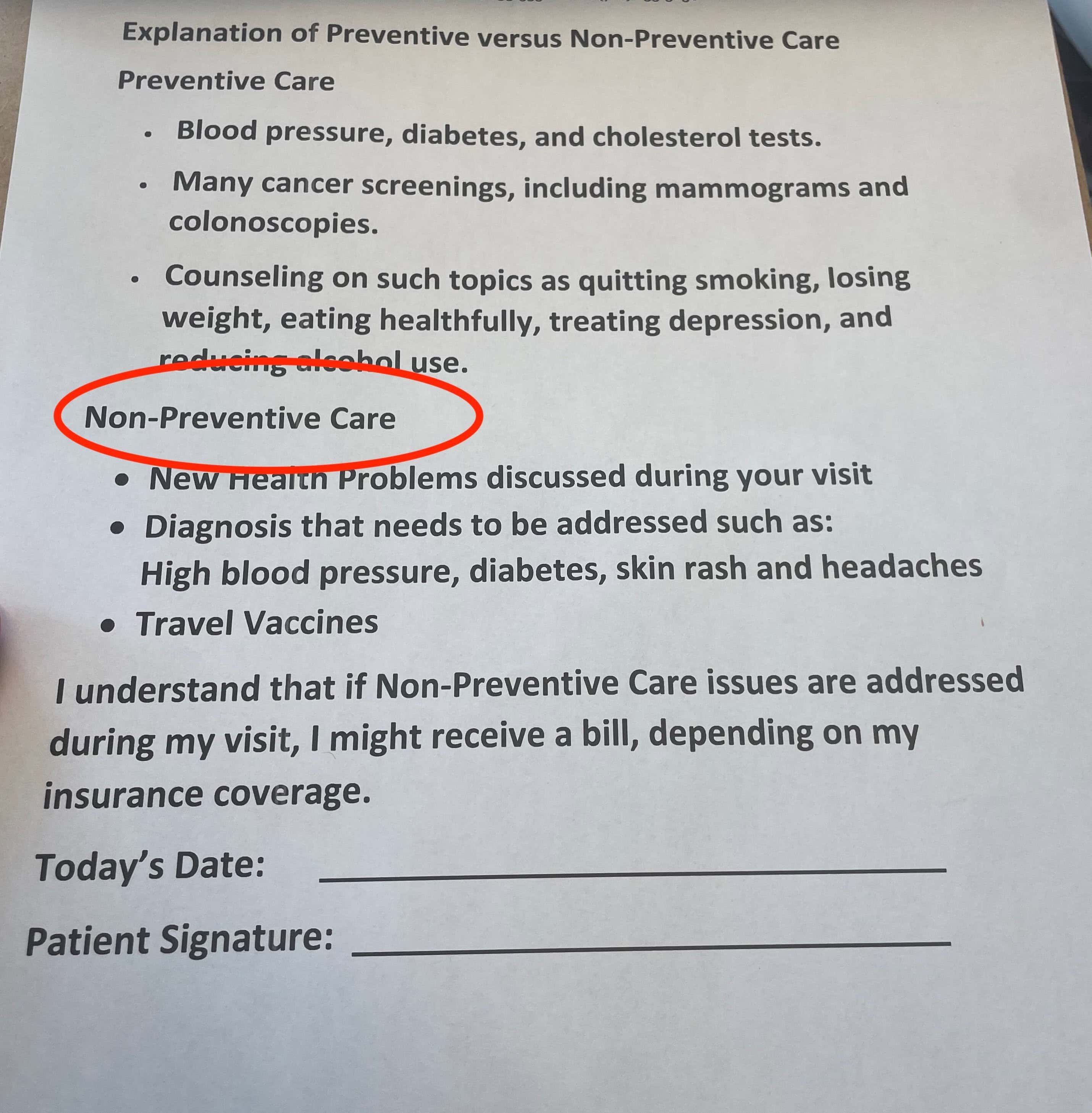

And even if you showed up just for the preventive stuff, you could get billed for a consult on issues that get diagnosed in a preventive screening, like high blood pressure.

That’s my takeaway from a form my doctor asked me to sign at my last annual checkup.

|

In the US health care system, talk is not cheap.

Your insurance isn’t governed by ACA rules.

Some health plans, like short-term plans, travel insurance, or what’s called “grandfathered plans” are exempt from these coverage requirements.

If you’re not sure whether your plan is grandfathered — and only about 14% of plans are — call your plan’s customer service number, or check with your HR department.

Things are wild, are vaccines still covered?

Short answer: yes. This year, anyway.

What’s considered “preventive” is based on guidelines issued by federal agencies.

And you’ve probably heard that some of those agencies have taken a notably anti-vaccine turn — controversially reducing the number of recommended childhood vaccines from 17 to 11.

But for now, private insurers have committed to covering all the vaccines that were recommended as of September 2025.

We’ve been following Katelyn Jetelina’s Substack Your Local Epidemiologist for updates on all things vaccine-related. KFF also has a useful tracker.

What to do if you get an unexpected bill

Follow the usual order-of-operations:

- Ask for an itemized bill and check whether you were billed for the right kind of service. If you weren’t — for instance, your provider billed something as diagnostic that you are positive was a preventive annual screening — call their billing office. Ask for them to re-submit the claim with the right billing code.

- If you were billed correctly, but your insurance isn’t covering the charge, make sure your plan is governed by the ACA — and not one of the “grandfathered” plans.

- If, like most people, you’re not in a “grandfathered” plan, refer to that list of covered services, and if they aren’t covering something they should (like polyp removal after a routine colonoscopy), file an appeal and demand that they do.

- And finally: If you know you need routine bloodwork or a scan — check with your insurance which labs are covered BEFORE your appointment, and ask your doc if your tests can be sent there ahead of time.

KFF Health News also has a handy guide for all this.

And we’re curious what you’re seeing out there as you get your check-ups. New forms to sign? Other surprises, or successes fighting back? Hit our inbox!

‘Till next week!

— Claire

P.S.: A previous version of this First Aid Kit newsletter said that Medicare covers a yearly physical for adults 65+ at no cost. In fact, Medicare covers “wellness visits” at no cost — which don’t include a physical exam, and are more like a consult with your doctor.

Get the First Aid Kit Newsletter!

Summing up the practical lessons we've learned about surviving the health-care system, financially.

Reporting on why health care costs so freaking much, and what we can maybe do about it.

More about us →

First Aid Kit

Get our latest tips for dealing with the healthcare-industrial complex.

Have a health care question?

For topic-specific deep dives and recommended reading, start here or use the search bar below to explore our site.